Using the plethora of data now available, here are 11 ways predictive analytics in P&C insurance will change the game in 2021. It developed a house view to codify critical underwriting considerations by industry segment and validated them through file reviews and historical analyses. /Using_advanced_analytics_to_identify_fraud_in_property_and_casualty_insurance.png?width=190&height=219&name=Using_advanced_analytics_to_identify_fraud_in_property_and_casualty_insurance.png) It then designed and piloted mechanisms to reinforce adherence to the house view as part of a broader quality program, and it set up a program management office to track execution of the remediation plan and assess its impact. Most insurance carriers limit their data and analytics efforts in underwriting to building specific use-case models and then revisiting these models every two or three years. P&C insurers can use predictive analytics to augment existing actuarial models and provide more personalized underwriting decisions.

It then designed and piloted mechanisms to reinforce adherence to the house view as part of a broader quality program, and it set up a program management office to track execution of the remediation plan and assess its impact. Most insurance carriers limit their data and analytics efforts in underwriting to building specific use-case models and then revisiting these models every two or three years. P&C insurers can use predictive analytics to augment existing actuarial models and provide more personalized underwriting decisions.

Securing adoption also requires tracking key performance indicators (KPIs) for underwriting and actively managing performance more broadly.

The Coalition of Insurance Fraud estimates that$80 billion is lost annually from fraudulent claims in the United States alone. Where humans fail, big data and predictive modeling can identify mismatches between the insured party, third parties involved in the claim (e.g.

1. Andy is a co-founder of Duck Creek Technologies and has been involved in the design and development of the solution offerings of the company. projected casualty underwriting collisionweek Yet insurance executives often cite human capitalnot financial capital or any other assetas their scarcest resource in the current business environment. The company continually assesses the value of various external data sources with respect to predictiveness, accuracy, and the like, and it drops those that provide unsatisfactory ROIs. Without predictive analytics, insurers could miss credible warning signs and lose valuable time that could be used to remedy any issues. How important is brand loyalty? Only when the solution is fully embedded in business as usual is the mission complete. Never miss an insight. After all, data is only a strategic asset when you can actually put it to work. The same insights can often be used in loss prevention. casualty insurers profitability worsen ratios

Only when the solution is fully embedded in business as usual is the mission complete. Never miss an insight. After all, data is only a strategic asset when you can actually put it to work. The same insights can often be used in loss prevention. casualty insurers profitability worsen ratios

JERSEY CITY, N.J., May 26, 2022 Despite experiencing an underwriting loss, the property/casualty insurance industry ended 2021 strong and able to support policyholders, according to a report from Verisk (Nasdaq: VRSK), a leading global data analytics provider, and the American Property Casualty Insurance Association (APCIA). And they conduct claims-trend analyses to identify product features that are proving more or less profitable than expected and that may warrant adjustments.

Insurers are also relying on insurance predictive modeling for fraud detection. In addition, predictive analytics in P&C insurance can help carriers to convert insights gained from customer-agent interactions, telematics, and even social media into credible foresights. insurance 2001 2003 celent casualty deal trends software edition property SS~` u{X#n$1)I3{IX}HZ`6ST _6r6UJx\}@F&1(g! Achieving underwriting excellence ultimately hinges on having highly trained and motivated staff. 5 0 obj We'll email you when new articles are published on this topic. P&C insurers should prioritize investments in predictive analytics, whether those be internal, external, or a combination of both. They have supplemented their monitoring of internal indicators with monitoring of external competitor data to help them determine when and where to make underwriting adjustments. Join 840,000+ CB Insights newsletter readers. Many consumers value a customized experience even when it comes to shopping for insurance. As with personal lines, use of advanced analytics and external data enables a disproportionately high share of STP, with only complex risks routed to underwriters for review.

With proper analytics tools, P&C insurers can review previous claims for similarities and send alerts to claims specialists automatically. A combination of factors, including significant unrealized capital gains, propelled policyholders surplus to a new record of $1,032.5 billion. casualty staking predictive Insurers have the option of using pre-built P&C insurance predictive analytics models or customizing their own models based on proprietary datasets. If youre already a customer, log in here.

Data is one of the most valuable assets an insurer can have, and predictive analytics has been helping businesses make the most of that data. Incorporating end users from the outsetusing design-thinking activities such as user-process interviews, ideation workshops, and usability testingnot only improves model designs but also facilitates their adoption by generating demand for them. This isnt exactly a new use for predictive analytics in insurance, but pricing and risk selection will see improvement thanks to better data insights in 2021. P&C insurance leaders are shifting more of their R&D budgets toward transformational innovation, focusing on novel technologies that can improve the efficiency and efficacy of underwriting processes.

Best-in-class performers invest in four activities aimed at setting up the organization for success with data and analytics initiatives. If the page has not redirected, please visit the 3E site here. Billion-dollar weather and climate disasters: Overview, National Centers for Environmental Information, 2021, ncdc.noaa.gov.

Best-in-class performers invest in four activities aimed at setting up the organization for success with data and analytics initiatives. If the page has not redirected, please visit the 3E site here. Billion-dollar weather and climate disasters: Overview, National Centers for Environmental Information, 2021, ncdc.noaa.gov.  You will soon be redirected to the 3E website.

But they can take advantage of advances in data and analytics to transform their underwriting and pricing operations. Data can reveal behavior patterns and common demographics and characteristics, so insurers know where to target their marketing efforts. How can CFOs rebrand themselves as innovation allies? Although insurers net earned premium increased 7.4% and surplus topped a trillion dollars, losses and loss adjustment expenses (LLAE) grew at an even faster rate to 11.1% in 2021, causing an underwriting loss for the year, said Robert Gordon, senior vice president, policy, research & international for APCIA.

You will soon be redirected to the 3E website.

But they can take advantage of advances in data and analytics to transform their underwriting and pricing operations. Data can reveal behavior patterns and common demographics and characteristics, so insurers know where to target their marketing efforts. How can CFOs rebrand themselves as innovation allies? Although insurers net earned premium increased 7.4% and surplus topped a trillion dollars, losses and loss adjustment expenses (LLAE) grew at an even faster rate to 11.1% in 2021, causing an underwriting loss for the year, said Robert Gordon, senior vice president, policy, research & international for APCIA.

Customers are always looking for fast, personalized service. series analysis Predictive analytics tools can anticipate an insureds needs, alleviating their concerns and improving their relationship with their carrier. Upskilling and reskilling underwriters is at least as important as attracting new talent. In the face of inflationary pressure that drives up claims costs, increasingly Top 10 Criteria for Selecting a Modern Core System Vendor. Keep the effort anchored in the C-suite; delegating down can dilute long-term aspirations. +*

Net underwriting gains declined to $1.8 billion from $4.9 billion in fourth-quarter 2020, and the combined ratio deteriorated to 100.0% from 98.2% a year prior. The insured losses from catastrophes in 2021, including Hurricane Ida in September, remained significant, even though associated net incurred losses and loss adjustment expenses declined to $56.3 billion in 2021 from $61.4 billion in 2020. And insurance was among the industries hardest hit by the massive economic contraction wrought by the pandemic. Indeed, McKinsey analysis has revealed that underwriting excellence is one of two key traits (along with pricing sophistication) that industry leaders have in common. }iVO'ONO*v5w5J_WY*K}#UwR/3=zR}+Y.VN~o2}>4=z"GA ]FW[-mz BfhWz4ZaykhoS*7V;2+/]/3o7}KkxE)hz+i And stay ahead. Leading insurance carriers use data and advanced analytics to reimagine risk evaluation, improve the customer experience, and enhance efficiency and decision making throughout the underwriting process. But with good predictive analytics systems, carriers will be able to prioritize certain claims to save time, money, and resources not to mention retain business and increase customer satisfaction. Since there are3.2 billion peopleon social media around the world, these platforms have become increasingly important when it comes to identifying potential markets. Historically, the complexity and heterogeneity of risks in this segment have made it challenging to use data and analytics to propel automation. Although the new approach still relies on input from human agents, a new STP risk-assessment engine minimizes manual effort. Net written premiums rose $13.8 billion, or 8.9%, compared to 2020. Some reports estimate its approximately10 MB of dataper household, per day, and that figure is expected to increase.

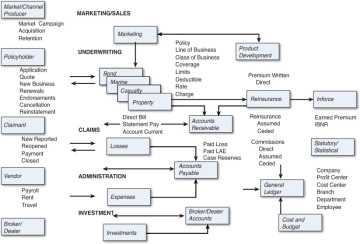

P&C insurance companies are always battling various instances of fraud, and oftentimes arent as successful as they would like. insurance flow property casualty overview industry analytics data figure informit

It then designed and piloted mechanisms to reinforce adherence to the house view as part of a broader quality program, and it set up a program management office to track execution of the remediation plan and assess its impact. Most insurance carriers limit their data and analytics efforts in underwriting to building specific use-case models and then revisiting these models every two or three years. P&C insurers can use predictive analytics to augment existing actuarial models and provide more personalized underwriting decisions. Securing adoption also requires tracking key performance indicators (KPIs) for underwriting and actively managing performance more broadly.

The Coalition of Insurance Fraud estimates that$80 billion is lost annually from fraudulent claims in the United States alone. Where humans fail, big data and predictive modeling can identify mismatches between the insured party, third parties involved in the claim (e.g.

1. Andy is a co-founder of Duck Creek Technologies and has been involved in the design and development of the solution offerings of the company. projected casualty underwriting collisionweek Yet insurance executives often cite human capitalnot financial capital or any other assetas their scarcest resource in the current business environment. The company continually assesses the value of various external data sources with respect to predictiveness, accuracy, and the like, and it drops those that provide unsatisfactory ROIs. Without predictive analytics, insurers could miss credible warning signs and lose valuable time that could be used to remedy any issues. How important is brand loyalty?

Only when the solution is fully embedded in business as usual is the mission complete. Never miss an insight. After all, data is only a strategic asset when you can actually put it to work. The same insights can often be used in loss prevention. casualty insurers profitability worsen ratios {kind=link}

JERSEY CITY, N.J., May 26, 2022 Despite experiencing an underwriting loss, the property/casualty insurance industry ended 2021 strong and able to support policyholders, according to a report from Verisk (Nasdaq: VRSK), a leading global data analytics provider, and the American Property Casualty Insurance Association (APCIA). And they conduct claims-trend analyses to identify product features that are proving more or less profitable than expected and that may warrant adjustments.

Insurers are also relying on insurance predictive modeling for fraud detection. In addition, predictive analytics in P&C insurance can help carriers to convert insights gained from customer-agent interactions, telematics, and even social media into credible foresights. insurance 2001 2003 celent casualty deal trends software edition property SS~` u{X#n$1)I3{IX}HZ`6ST _6r6UJx\}@F&1(g! Achieving underwriting excellence ultimately hinges on having highly trained and motivated staff. 5 0 obj We'll email you when new articles are published on this topic. P&C insurers should prioritize investments in predictive analytics, whether those be internal, external, or a combination of both. They have supplemented their monitoring of internal indicators with monitoring of external competitor data to help them determine when and where to make underwriting adjustments. Join 840,000+ CB Insights newsletter readers. Many consumers value a customized experience even when it comes to shopping for insurance. As with personal lines, use of advanced analytics and external data enables a disproportionately high share of STP, with only complex risks routed to underwriters for review.

{kind=link}

With proper analytics tools, P&C insurers can review previous claims for similarities and send alerts to claims specialists automatically. A combination of factors, including significant unrealized capital gains, propelled policyholders surplus to a new record of $1,032.5 billion. casualty staking predictive Insurers have the option of using pre-built P&C insurance predictive analytics models or customizing their own models based on proprietary datasets. If youre already a customer, log in here.

{kind=link}

Data is one of the most valuable assets an insurer can have, and predictive analytics has been helping businesses make the most of that data. Incorporating end users from the outsetusing design-thinking activities such as user-process interviews, ideation workshops, and usability testingnot only improves model designs but also facilitates their adoption by generating demand for them. This isnt exactly a new use for predictive analytics in insurance, but pricing and risk selection will see improvement thanks to better data insights in 2021. P&C insurance leaders are shifting more of their R&D budgets toward transformational innovation, focusing on novel technologies that can improve the efficiency and efficacy of underwriting processes.

Best-in-class performers invest in four activities aimed at setting up the organization for success with data and analytics initiatives. If the page has not redirected, please visit the 3E site here. Billion-dollar weather and climate disasters: Overview, National Centers for Environmental Information, 2021, ncdc.noaa.gov. Customers are always looking for fast, personalized service. series analysis Predictive analytics tools can anticipate an insureds needs, alleviating their concerns and improving their relationship with their carrier. Upskilling and reskilling underwriters is at least as important as attracting new talent. In the face of inflationary pressure that drives up claims costs, increasingly Top 10 Criteria for Selecting a Modern Core System Vendor. Keep the effort anchored in the C-suite; delegating down can dilute long-term aspirations. +*

{kind=link}

Net underwriting gains declined to $1.8 billion from $4.9 billion in fourth-quarter 2020, and the combined ratio deteriorated to 100.0% from 98.2% a year prior. The insured losses from catastrophes in 2021, including Hurricane Ida in September, remained significant, even though associated net incurred losses and loss adjustment expenses declined to $56.3 billion in 2021 from $61.4 billion in 2020. And insurance was among the industries hardest hit by the massive economic contraction wrought by the pandemic. Indeed, McKinsey analysis has revealed that underwriting excellence is one of two key traits (along with pricing sophistication) that industry leaders have in common. }iVO'ONO*v5w5J_WY*K}#UwR/3=zR}+Y.VN~o2}>4=z"GA ]FW[-mz BfhWz4ZaykhoS*7V;2+/]/3o7}KkxE)hz+i And stay ahead. Leading insurance carriers use data and advanced analytics to reimagine risk evaluation, improve the customer experience, and enhance efficiency and decision making throughout the underwriting process. But with good predictive analytics systems, carriers will be able to prioritize certain claims to save time, money, and resources not to mention retain business and increase customer satisfaction. Since there are3.2 billion peopleon social media around the world, these platforms have become increasingly important when it comes to identifying potential markets. Historically, the complexity and heterogeneity of risks in this segment have made it challenging to use data and analytics to propel automation. Although the new approach still relies on input from human agents, a new STP risk-assessment engine minimizes manual effort. Net written premiums rose $13.8 billion, or 8.9%, compared to 2020. Some reports estimate its approximately10 MB of dataper household, per day, and that figure is expected to increase.

P&C insurance companies are always battling various instances of fraud, and oftentimes arent as successful as they would like. insurance flow property casualty overview industry analytics data figure informit

{kind=link}